With 2020 just around the corner, financial services is coming to a critical juncture in how it uses data and presents itself to the general consumer.

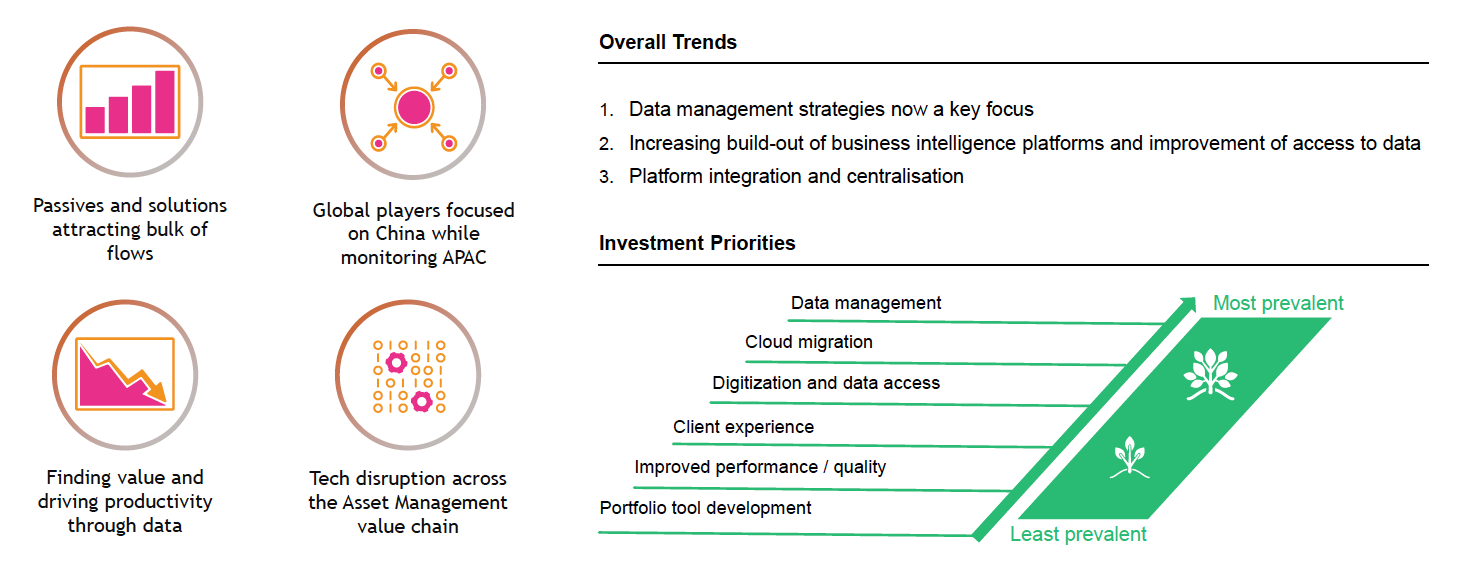

In a recent presentation from the Investment Association (IA) on global mega trends, platform centralisation was one of the critical issues that the industry needs to contend with.

So, why are platform integration and centralisation so crucial for financial services? And what do they really mean in practice?

Taking a step back, consumers now demand and expect a seamless service and this has been a large part of the success behind Silicon Valley giants such as Amazon, Apple and Google that have transformed the corporate world. With access to, and intuitive use of, thousands of terabytes of data, these companies cultivate groundbreaking experiences for their customers. They have undoubtedly raised the standards of customer service and deliverance to impossible highs, so why don’t we have the same with our financial services?

One could argue that due to its inherently conservative nature, financial services has been slow to embrace change and in particular has been reluctant to embrace technology at times. This has changed in recent years (partly led through consumer appetites and partly forced via regulation) and nearly all the leading names have an online presence.

*Source: The Investment Association and BCG Expand Research

With thousands of FinTech firms nipping at the heels of the incumbents, even the largest firms now offer digital interfaces and apps for their consumers. Greater access to technology has put more pressure on the intermediary in any business relationship (I.e. Uber and AirBnB), and financial services is also moving in this direction. But it goes deeper than this.

PwC expects this to come to a head in 2020 and predicts a demand from each customer for a seamless, integrated and tailored solution. Furthermore, the firm expects most asset managers to have a Chief Digital Officer in the next 18 months.

Therefore, this goes further than simply having an app but instead drives at the very heart of how these firms use data in what they do. For instance, overall consumers trust the largest brands and how they use their data to market to them – whenever a regular Amazon user logs onto the site, they expect that website to know what deals and products they are looking for. What’s more, they have implicit trust that their payment will be quickly and securely processed and that an automated warehouse somewhere will instantly have their product packaged and on its way within minutes. This seamless offering is a large part of the reason consumers keep coming back.

And we have already seen this in financial services to some extent. For instance, in 2013, Chinese online payment platform Alipay launched an online money market fund, Tu’E Bao that now makes Tianhong Asset Management Co. the second largest asset manager in China. It was successful, in part, due to the strong trust of the general public, to being an affiliate of a technology company and to providing a tailored product.

Elsewhere, change has been slow but is definitely happening. The demand for a seamless and all-in-one service has driven corporate M&A activity and in the UK many asset managers have been busy establishing (or acquiring) their own financial planning arms and ensuring they are more than just product providers. Millions, perhaps billions, has been spent by firms desperate to own as much of the customer relationship as possible (and to drive down prices wherever they can).

*Source: The Investment Association

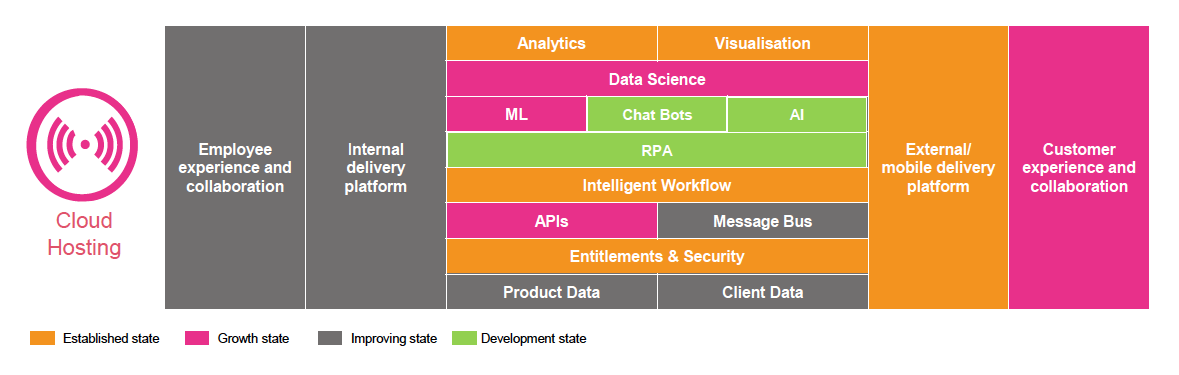

However, this is arguably only as good as how the data is used. This follows through from the front office (marketing, customer service, communications etc), through to deal and trade execution right through to the back office (concerning administration efficiency, compliance, oversight etc). In the end, success won’t come down to who has the most data or the biggest cloud. Instead, who is offering the best service with it, marketing with the strongest personalisation and essentially delivering a level of experience that is already being received in nearly all other areas of commerce?

This brings us back to the issue of platform integration and centralisation. There have been some high-profile debacles within UK financial services when it comes data and the dreaded issue of ‘replatforming’, with many shareholder-conscious management teams wary about overhauling their data management systems while staying competitive. But in the long run these brands will increasingly face questions and heightened demands when it comes to the use of data.

At MirrorWeb, we have honed in on one part of this data puzzle and several leading names in the financial services industry are already using our solution as a result. Our scalable and secure platform ensures firms have a reliable and regulatory-complaint archive of their data and their digital presence. With such a growing emphasis on what appears on their website, and who it is targeted at, every day new firms are getting in touch to see how a more sophisticated solution can give them compliance peace of mind.

Want to find out more about MirrorWeb?

At MirrorWeb, we have honed in on one part of this data puzzle and several leading names in the financial services industry are already using our solution as a result. Our scalable and secure platform ensures firms have a reliable and regulatory-complaint archive of their data and their digital presence. With such a growing emphasis on what appears on their website, and who it is targeted at, every day new firms are getting in touch to see how a more sophisticated solution can give them compliance peace of mind.

Keen to find out more? Simply request a demo of the MirrorWeb Platform by clicking the button below…

.png?width=352&name=surveillance%20blog%20v2%20(1).png)